Transforming the way banks interact with customers

By 2023, the majority of organizations using AI for digital commerce will achieve at least a 25% improvement in customer satisfaction, revenue or cost reduction, Gartner says.

Personal banking service delivers a better customer experience across human and digital channels. Here’s how:

- Marketing with focus. Consumers face a gulf of marketing and will quickly tune out messages that are not relevant. Personal banking that’s enabled by technology ensures that institutions do not become part of the noise by reducing the degree of irrelevant offers. Instead, personal banking delivers highly relevant, effective marketing that grows the customer relationship.

- Enabling omnichannel. Though retail banking is less and less branch-based customers still interact with their banks across multiple channels – including the branch. Technology helps banks deliver relevant, personal services irrespective of the channel a customer prefers at any given point in time.

- Recommended actions. Financial services can be a challenging topic for many consumers. Tech helps banks drive recommendations, including suggested next best actions that guide consumers through their complex financial affairs. In doing so institutions retain customers while building a greater degree of trust.

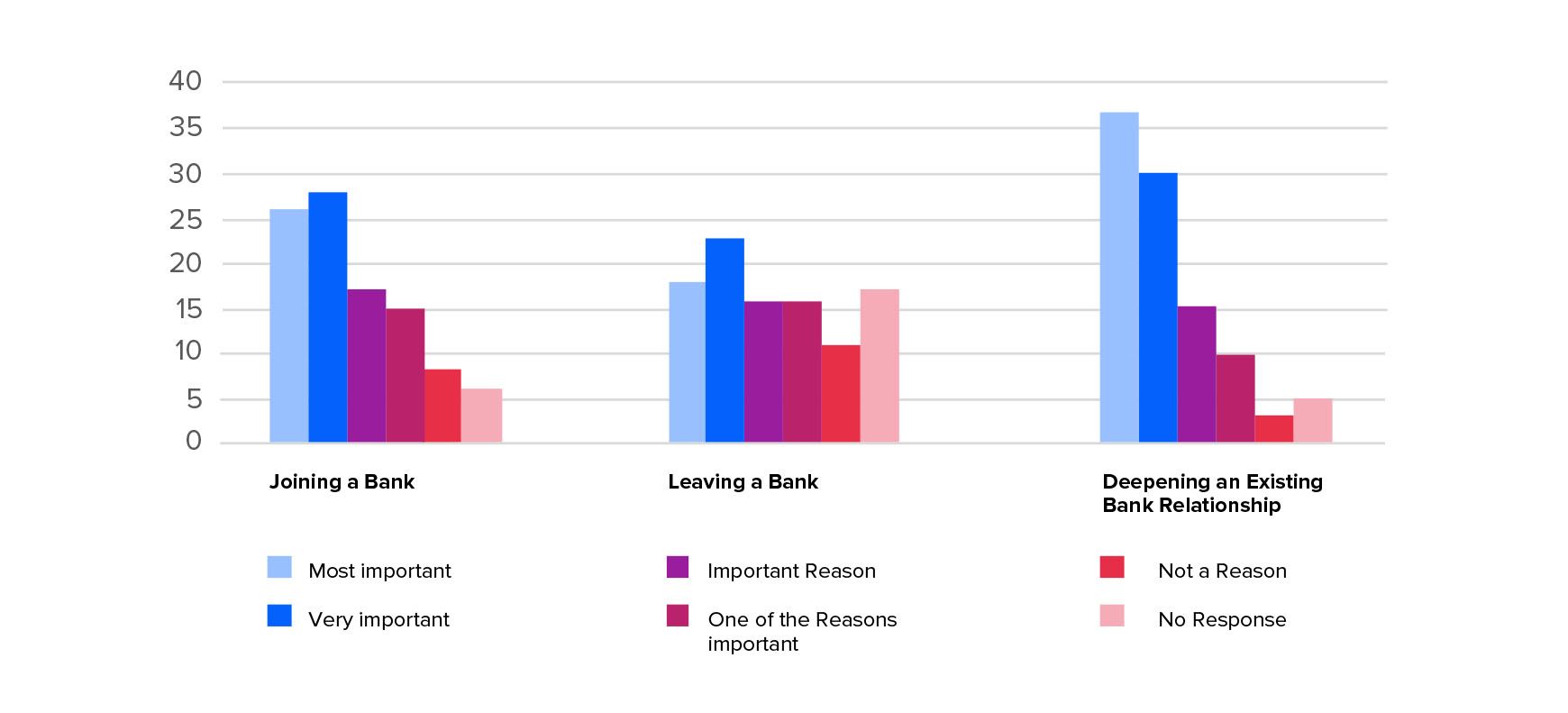

Consumers may rarely change banks. Nonetheless they frequently interact with their banks. A bank stands to lose substantially if and when customers decide to switch. Furthermore, banks that can build a reputation for personalized banking will enjoy big wins as new customers sign up thanks to referrals.

Personalisation vs compliance and security

There is, however, a real hurdle when it comes to rolling out personalised retail banking. A tightening compliance and security environment makes the level of data sharing and processing required by personalized banking much more challenging than it would otherwise be.

And, of course, the most personal banking service in the world can quickly be undermined if consumers fail to trust a financial institution. Banks need to remain cognizant of three key areas:

- Data sharing can expose institutions to cyber threats, banks should beef up cybersecurity to ensure open banking does not result in data loss.

- Throughout driving individualised banking services institutions need to stay on the right side of compliance law.

- In the journey to more personal banking institutions should be careful to not get to the point of invading induvial privacy.

That said, with the right measures in place banks can deliver incredibly personal experiences without exposing consumer’s trust to any degree of risk.

At ELEKS, we have assisted countless financial institutions, including banks, to make the best use of digital innovation. Get in touch with us to find out how we can harness Data Science and latest fintech trends to deliver a more personal banking experience across your customer base.

Related Insights